Mobile DRAM

|

|

Mia Huang, Research Manager at DRAMeXchange, covering trends of mobile DRAM in 2018 (Image: LEDinside) |

Mobile DRAM prices have been going up since 3Q16, and the main specifications saw an average price growth of around 40% up to now. The price hike not only led to smartphones vendors’ decreased profits, but also lowered their intention to improve the memory content of phones. In 2018, DRAM suppliers will not carry out large-scale capacity expansion plans, so the increase in DRAM supply will be limited and prices will remain high. Consequently, brands need to reconsider their production planning for cost-based pricing models, and to carefully assess their marketing strategy of promoting low-price models in emerging market. The average memory content for smartphones will also grow slower due to increasing mobile DRAM price. The launch of new iPhone will be a main drive of the memory content growth.

Server

|

|

Mark Liu, Analyst at DRAMeXchange, shared the development of server shipment. (Image: LEDinside) |

TrendForce forecasts global server shipments to register a growth of 5.3% in 2018; HPE, Dell, and Lenovo will remain the top 3 vendors, jointly accounting for a shipment market share of 40%. As smart end-applications and devices grow more popular, data center ODM Direct will be the largest driver of server demand in 2018, recording a 14.4% shipment growth. Currently, memory suppliers’ shipment fulfillment rates are only around 70% to 80% due to a persistent undersupply of server DRAM. Due to procurement contracts in China in 1H18 and the arrivals of Purley-bases servers, demand for high-capacity server modules will keep going up till the end of next year. So the prices of mainstream modules will stay high.

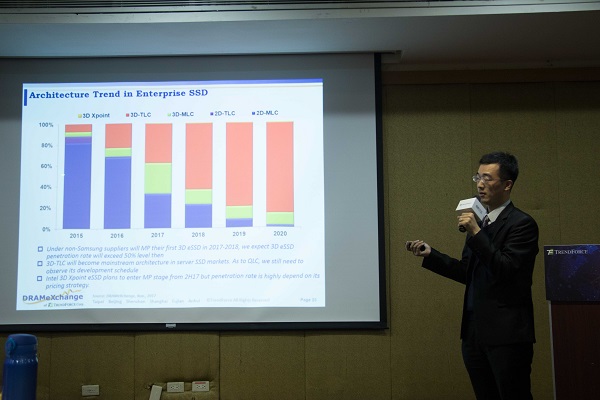

NAND Flash

|

|

Alan Chen, Senior Research Manager at DRAMeXchange, explained seasonality factors affecting NAND Flash suppliers. (Image: LEDinside) |

Demand has exceeded supply in the global NAND Flash market since 2H16, and the undersupply was not eased until 4Q17. As for 2018, traditional off-peak season in the first half of year will cause the NAND Flash demand to drop, resulting in a slight oversupply and price drop. However, as the demand bounces back in 2H18, and NAND Flash suppliers have conservative production capacity expansion, the market may experience undersupply again as the result, and the price is not likely to keep going down. NAND Flash ASP will have a 10% to 20% drop (YoY) in 2018. UFS transfer interface has chance to enter the low- and mid-range market of smartphones, achieving a penetration rate of 20%. On the other hand, benefited from increasing attach rate for SSDs into server, data center and PC, SSDs will be a major demand driver for NAND Flash, accounting for more than 40% of the overall NAND Flash output in 2018. Particularly, PCIe interface will be a mainstream. In addition, the penetration rate of NB SSD has chance to reach over 50% as the NAND Flash price decreases.

Large-Size Panel

|

|

Iris Hu, Research Manager at WitsView, debunked China would rise as the largest OLED supplier. (Image: LEDinside) |

The first Gen 10.5 fab worldwide, owned by China’s BOE Technology (BOE), will be entering mass production at the end of 1Q18. This fab will not only become the world’s largest-generation panel fab, but also enable BOE to achieve a new high of shipments. The Gen 10.5 fab is for production of large-size (65" & 75") TV panels. In response, Korean and Taiwanese panel makers have already increased their shipments of 65" and 75" panels in advance, totaling 11 million and 1.6 million units in 2017 respectively. Particularly, the YoY growth of 75" panel shipment is estimated to reach 123.6%, indicating the substantial impacts of Gen 10.5 fab on the global panel industry. As for IT panels, the market has become saturated and in order to boost demand, panel makers have improved specs and switched to borderless design. Consequently, the demands for monitor and notebook panels are estimated to increase in 2018. Overall, as panel makers continue to increase production capacity in 2018, the panel market will experience an oversupply, thus leading to a continuous drop in panel prices. However, lower panel prices will be lead to more product promotion from brands. As a result, TrendForce estimates large-size panel demand and supply by area will grow by 7% and 7.7% respectively in 2018. As the market demand increases, the glut ratio for large-size panels will also change from 7.8% to a more balanced figure of 5.2%.

Small-Size Panel

|

|

Boyce Fan, Research Director at WitsView, estimated the market share growth of OLED companies in the smartphone market. (Image: LEDinside) |

The launch of iPhone X has brought major influences to the smartphone market. For instance, the transition from TFT-LCD to AMOLED panels has led to a new wave of investment in AMOLED production capacity, especially from Chinese panel makers. As the exclusive supplier of iPhone AMOLED panel, Samsung Display (SDC) is the current market leader in terms of technology and production capacity of AMOLED panels. However, SDC still faces the competition from rivals like LGD and BOE in the future. Regarding small- and middle-size AMOLED production capacity by area, TrendForce estimates that the share of South Korean panel makers in the overall capacity will drop to 66% while that of China-based makers will increase to 23% in 2020, at the earliest. In addition, although panel makers and IC design houses actively raise the portion of In-Cell solutions integrated with TDDI chips in the smartphone market, the future growth of In-Cell solutions will be influenced by decreased demand from Apple as it shifts to AMOLED panels for its handsets. The share of In-Cell solutions in the smartphone market is estimated at 25.5% in 2018. Last, smartphones featuring the full-screen, 18:9 or above aspect ratio display have been rolled out in 2017. Panel makers have thus started mass production of 18:9 panels in the second half of this year. Due to promotional efforts from smartphone brands, the penetration of 18:9 devices will take off in 2018 with rate forecast at 39.6%.

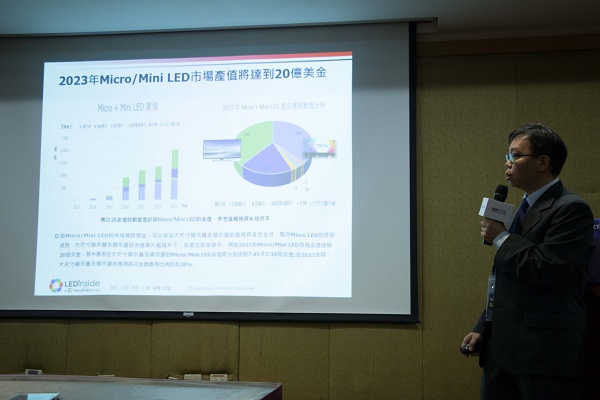

Micro LED

|

|

Simon Yang, Assistant Research Manager at LEDinside, projected the market value of Micro/Mini LED would hit USD 2 billion by 2023. (Image: LEDinside) |

Apple acquired micro LED specialist LuxVue in 2014 and became the owner of the most Micro LED technology and patents worldwide, making the Micro LED a focus for the market. However, Micro LED is still in the early stage of development due to critical technological bottlenecks, including mass transfer, uniformity of epitaxial layer, electric current control, full-color emission, etc. With superior performance, Micro LED can be used in smart watch, smartphone, automotive display, AR/VR, digital display and TV, etc. But considering its high technological barriers and high cost, Micro LED is more suitable for high-end TV, display, and automotive display. In the future, large-size display and digital display will be mainstream products as they are expected to register higher revenue.