Ad hoc announcement pursuant to Art. 53 Listing Rules of SIX Swiss Exchange

-

Q4/23: revenues of EUR 908 million, above midpoint of the guidance range

-

Q4/23: adj. EBIT margin of 6.9%, or EUR 62 million, above the midpoint of the guided range

-

Q1/24: expected first quarter 2024 revenues of EUR 800 to 900 million with adj. EBIT margin of 4% – 7% driven by usual seasonality and weak industrial & medical market

-

FY/23: revenues of EUR 3.59 billion

-

FY/23: adj. EBIT margin of 6.5%, or EUR 233 million

-

Continued strong design-win traction for structural growth, particularly in automotive

Premstaetten, Austria, and Munich, Germany (9 February 2024) -- ams OSRAM (SIX: AMS) delivers solid Q4 with revenues at EUR 908 million and adjusted EBIT of 6.9%, above the midpoint of the guided range, revenues of EUR 3.59 billion and 6.5% adj EBIT for Fiscal Year 2023. ams OSRAM continues executing its ‘Re-establish-the-Base’ efficiency and strategic realignment program to benefit from structural growth. The plan is underpinned by a strong design-win pipeline.

“We kept our promise and have achieved a lot in 2023: defined a new strategy, implemented a new organization, secured the re-financing and strengthened the balance sheet. We are now ready to deliver the turnaround and benefit from structural growth in our core markets in automotive, industrial, medical and dedicated consumer applications. On the back of a very solid Q4 2023, we are confident to be able to execute our plans for 2024 and make ams OSRAM a more focused, leaner, and more efficient company driven by relentless innovation and sustainable partnerships with our customers.” said Aldo Kamper, CEO of ams OSRAM.

Q4/23 financial and business update

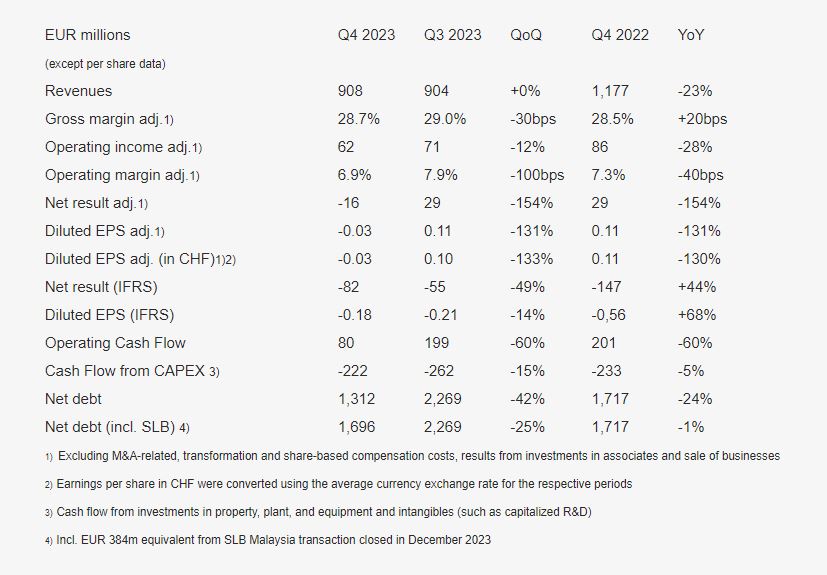

ams OSRAM announces revenues of EUR 908 million for the fourth quarter, slightly above the midpoint of the guided range of EUR 850 – 950 million, a 4 million EUR increase compared to the previous quarter. The adjusted EBIT (adjusted earnings before interest and taxes, i.e. operating margin adjusted for special, non-operational effects) margin came in above the midpoint of the guided range of 5% - 8%, namely at 6.9%. The adjusted EBIT amounted to EUR 62 million. The company continues to win new business across the board underpinning its structural growth plans, especially in automotive. The company progresses with preparing the exit of the non-core semiconductor portfolio (with 2023 run-rate of around EUR 300 to 400 million) with focus on its passive optical components business.

Semiconductor segment update

The Semiconductor segment represented 69% of Q4 revenues, or correspondingly EUR 629 million. End-markets continued to show a diverse pattern.

Automotive:

Demand for products for automotive applications was particularly strong from China, whilst the other regions showed normal seasonal demand. Overall, the company recorded the highest ever revenue number from automotive semiconductor products, namely EUR 278 million, a 10% year-over-year increase. It underlines the strength of its underlying market position in its markets. Quarter-over-quarter, revenues increased by 7%.

Industrial & Medical (I&M):

Industrial and medical markets remained cyclically weak, with often significantly lower run-rates compared to a year before. Revenues declined both quarter-over-quarter and year-over-year. Demand from professional and industrial lighting applications was particularly soft. Project activity and thus demand for its Hyper Red LED products for horticulture continued to be below normal seasonality. Mass-market revenues – representing a very broad variety of applications - showed much lower traction than a year ago. Consequently, channel inventories remained at a high level.

Consumer:

Revenues from products for personal consumer devices showed a mixed picture. Shipments into Android based devices improved quarter-over-quarter on the back of stronger shipments of mid-end to premium Android smartphones during Q4, where ams OSRAM holds leading positions in its product categories. Overall, the company saw lower sales in consumer applications both, quarter-over-quarter and year-over-year. This development is due to ramp down of lost design sockets that used to be large revenue contributors in previous years.

The adjusted EBIT in the semiconductor segment landed at EUR 29 million, representing a 4.6% adj. EBIT margin, compared to EUR 36 million, or 5.6% adj. EBIT margin in the previous quarter. On a like-for-like basis, the adj. EBIT improved quarter-over-quarter, considering the reported one-time effect in Q3 (funding catch-up effect).

Lamps & Systems segment update

The Lamps & Systems segment represented 31% of Q4 revenues, or correspondingly EUR 279 million. In both automotive and industrial & entertainment markets, business performed as expected.

Automotive:

Aftermarket sales came in as strong as seasonally expected. The company typically sees its strongest demand in Q4 and Q1 when high halogen bulb replacement rates can be expected in Europe and North America.

Specialty Lamps:

Due to high inventories at customers, the demand for high-performance lamps for semiconductor equipment remained weak. Other markets were muted, too.

The adjusted EBIT in the Lamps & Systems segment stood at 33 million Euro in Q4, or 11.9% adjusted EBIT margin, correspondingly. The quarter-over-quarter decline was due to an adverse one-time raw material effect, impacting profitability negatively by a mid single digit million Euro figure. Excluding this effect, adj. EBIT margin would have come in stronger than in the previous quarter.

Quarterly financial summary

Considering the reported positive one-time effects in the previous quarter, adjusted Gross and Operating margins stayed essentially flat, quarter-on-quarter. The average EUR/USD exchange rate stood at 1.09.

The adjusted net result came in at minus EUR 16 million due to a significantly more negative net financing result in Q4 as a consequence of the EUR 2.25 billion re-financing effective in Q4.

On December 7th, the company completed its EUR 808 million rights issue. The number of shares increased from 274,289,280 to 998,443,942. Consequently, the average share count in Q4 stood at 456,490,225, which is the relevant reference for the earnings per share calculation in Q4.

Fourth quarter adjusted diluted earnings per share came in at minus EUR 0.03 compared to EUR 0.11 in the previous quarter.

Operating cash flow came in at EUR 80 million in Q4 2023 compared to EUR 199 million in Q3. A reduction of trade payables mostly relating to Capex amongst other factors contributed to this development.

The balance sheet was strengthened as a result of the capital raise and the associated repayment of outstanding long-term debt instruments that were due in 2025. Consequently, the net debt position significantly improved from EUR 2,269 million in Q3 to EUR 1,696 million in Q4 when including EUR 384 million equivalent from the Sale-and-Lease Back Malaysia transaction.

FY23 financial and business update

In Fiscal Year 2023, the new management team around Aldo Kamper (CEO) and Rainer Irle (CFO) gave the company a new strategic direction, initiated its ‘Re-establish the Base’ turnaround program targeted to focus the portfolio, make the company leaner and more efficient in bringing innovation to market. Furthermore, the midterm target operating model was updated and the balance sheet strengthened. All these developments are setting the base for structural growth from the core portfolio of intelligent emitter and sensor components in automotive, industrial, and medical markets. The company will continue to pursue dedicated semiconductor business in consumer applications focusing on technologies where it can differentiate on a sustainable basis. The Lamps & Systems segment will remain a significant contributor to profit and cash generation.

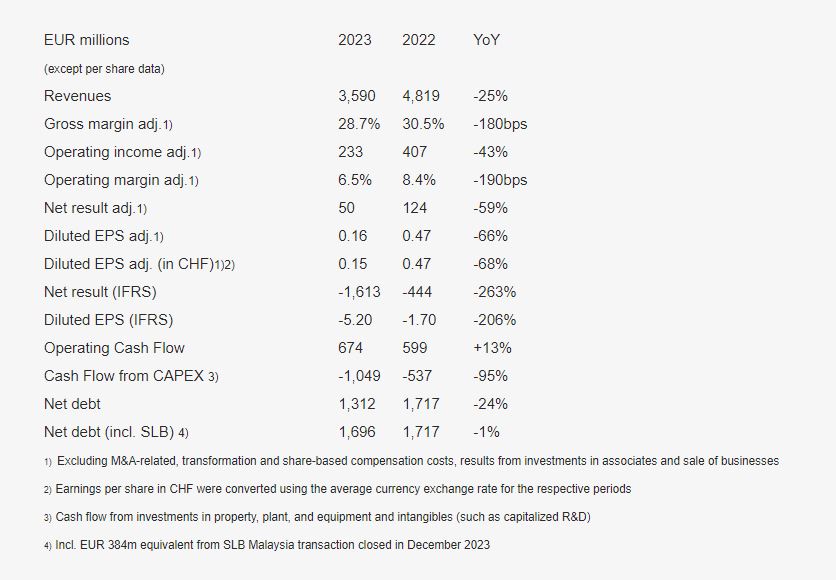

In Fiscal Year 2023, ams OSRAM recorded revenues of EUR 3.59 billion after EUR 4.82 billion in fiscal year 2022. The decline of 25% was driven by portfolio divestitures in the Lamps & System segment (around EUR 500 million) and a contraction in the Semiconductor segment. Within the latter, the dominant factor was the ramp down of major programs with components for smartphones after those design sockets had been lost, besides the cyclical inventory correction in the automotive (in H1 2023) segment and a severe market weakness in certain industrial segments, such as horticulture or professional lighting.

Adjusted EBIT for fiscal year 2023, came in at EUR 233 million after EUR 407 million in the previous fiscal year. The key driver for this development were underutilization cost in the semiconductor business for consumer device applications that are no longer core and underutilization cost for products in industrial and automotive applications in the wake of the inventory corrections.

Full year adjusted diluted earnings per share were EUR 0.16 or CHF 0.15 and EUR -5.20 or CHF -5.06 unadjusted.

Operating cash flow stood at EUR 674 million in FY 2023, after EUR 599 million in FY2022. CAPEX was much higher year-over-year on an exceptional basis, driven by the extraordinary investment in disruptive, 8-inch based microLED technology for a new generation of brighter, more efficient, self-illuminating displays.

FY23: re-financing completed ahead of schedule

On September 27th, 2023, the company announced its comprehensive financing plan to address the then outstanding maturities in 2025 and to strengthen the balance sheet. The company raised in total approximately EUR 2.25 billion, via the rights issue around EUR 800 million, the upscaled issuance of new senior unsecured notes due to high market demand of around EUR 1 billion and a sale & lease-back transaction besides divesting a phased-out production facility which together yielded around EUR 450 million. Given the upscaled amounts in 2023, a final smaller tranche in 2024 is thus no longer needed and the company completed its re-financing ahead of schedule.

FY23: mid-term target financial model

In 2023, the company also updated its mid-term target financial model. On a like-for-like basis (without the non-core portfolio in semiconductors of EUR 300 to 400 million in 2023), the company targets to grow 6% to 10% CAGR, underpinned by a strong design-win base, and targets an adjusted EBIT margin of around 15% by 2026.

The model is also underpinned by the company’s expectation of a normalization of the CAPEX to sales ratio of around 10% by 2025, following completion of the above average investment cycle of recent years tied to the investments into the new 8-inch capabilities, thereby further improving its free cash flow. The full implementation of the ‘Re-establish the Base’ program, which is expected to deliver approximately EUR 150 million run-rate improvements of adjusted EBIT by the end of FY2025 will contribute sustainably to the cash flow generation ability going forward.

FY23: Progress of Reestablish-the-Base Program

On July 27th, 2023, the company announced its ‘Re-establish the Base’ program, focusing on its profitable core as a new base for sustainable, profitable growth.

In terms of portfolio measures aimed at exiting certain non-core businesses in the semiconductor portfolio, the company has prioritized the carve-out of the passive optical components business and a second product line.

In terms of ‘monetizing innovation’, the company has completed the consolidation in the semiconductor segment from 3 business units to 2 as of October 1st, 2023, strengthening the accountability of the business units for streamlined end-to-end business performance.

Effective, January 1st, 2024, the management board consists of 2 members (CEO and CFO), compared to 4 members one year ago.

FY23: Strong Design-Win performance in Fiscal Year

The company could continue to win meaningfully new business during fiscal year 2023. The combined figure came in above EUR 5 billion across all segments of its core semiconductor portfolio. The largest contribution came from automotive.

Status of outstanding OSRAM minority shares

On December 31st, 2023, the Group held around 86% of OSRAM Licht AG shares, compared to 86% on September 30th, 2023. The total liability for minority shareholders’ put options stood at EUR 611 million at the end of Q4/2023 compared to EUR 616 million at the end of Q3/2023.

The company has an undrawn Revolving Credit Facility (RCF) of EUR 800 million in place, which was prolonged to September 2026 with the successful execution of the rights issue in December 2023. The RCF is primarily in place to cover any further significant exercises under the 'domination and profit and loss transfer agreement (DPLTA)’ put option.

First Quarter 2024 Outlook

The company continues to see weak demand from industrial and medical markets. Demand from consumer device application markets remains modest, in spite of some recent uptick in smartphone related demand. As a result, the Group expects first quarter revenues to decline in line with typical seasonality, pronounced by weakness in industrial & medical markets in a range of EUR 800 – 900 million. Demand from China for its automotive semiconductor products is expected to normalize, as well. The adjusted EBIT is expected to come in accordingly, in line with typical fall-through, at 4% to 7%. The EUR/USD exchange rate is assumed at 1.08.

Comments on FY 2024

In terms of business dynamics, ams OSRAM expects sustained weakness – partly driven by inventory corrections - in the industrial and medical segments during the first half. The company expects some improvement in the second half of the year, driven by new business wins and a potential normalization in the industrial and medical segment.

Within the context of its ‘Re-establish-the-Base’ program, the company expects to exit certain non-core semiconductor businesses with EUR 300 to 400 million of 2023 revenues. In 2024, the run-rate of these non-core businesses will be lower as some of these businesses are phasing out gradually. For FY2024, the company has prioritized the carve-out of the passive optical components business and a second product line.

The ‘Re-establish-the-Base’ program is expected to deliver approximately EUR 75 million run-rate improvements to adjusted EBIT at the end of FY2024. In contrast to these improvements, the company expects back to normal annual price declines and higher personnel cost in view of last year’s high inflation rates besides significant ramp-up cost for its new 8-inch led facility in Kulim, Malaysia.

The company continues to expect positive free cash flow (including divestment proceeds) in 2024.

Additional Information

Additional financial information for the fourth quarter as well as 2023 is available on the company website. The fourth quarter 2023 investor presentation incl. detailed information is also available on the company website. ams OSRAM will host a press call as well as a conference call for analysts and investors on the fourth quarter results on Friday, 09 February 2024. The conference call for analysts and investors will start at 9.00am CET and can be joined via webcast. The annual press conference and call will take place at 10.30am CET.

About ams OSRAM

The ams OSRAM Group (SIX: AMS) is a global leader in intelligent sensors and emitters. By adding intelligence to light and passion to innovation, we enrich people’s lives.

With over 110 years of combined history, our core is defined by imagination, deep engineering expertise and the ability to provide global industrial capacity in sensor and light technologies. We create exciting innovations that enable our customers in the automotive, industrial, medical and consumer markets to maintain their competitive edge and drive innovation that meaningfully improves the quality of life in terms of health, safety and convenience, while reducing impact on the environment.

Our around 20,000 employees worldwide focus on innovation across sensing, illumination and visualization to make journeys safer, medical diagnosis more accurate and daily moments in communication a richer experience. Our work creates technology for breakthrough applications, which is reflected in over 15,000 patents granted and applied. Headquartered in Premstaetten/Graz (Austria) with a co-headquarters in Munich (Germany), the group achieved EUR 3.6 billion revenues in 2023 and is listed as ams-OSRAM AG on the SIX Swiss Exchange (ISIN: AT0000A18XM4).

Gold+ Member Report

Gold+ Member Report

|

Report Title

|

Content

|

Format

|

Publication

|

|

LED Industry Demand

and Supply Database

|

Demand Market Analysis:

|

PDF / Excel

|

1Q (Mid Mar.)

3Q (Early Sep.)

|

|

2024-2028 Demand Market Forecast

|

|

(Backlight and Flash LED / General Lighting / Agricultural Lighting / Architectural Lighting / Automotive- Passenger Car & Box Truck & Scooter / Video Wall / UV LED / IR LED / Micro LED / Mini LED)

|

|

Supply Market Analysis:

|

|

1. LED Chip Market Value (External Sales, Total Sales)

|

|

2. WW New / Accumulated GaN LED and AS/P LED MOCVD Chamber Installations

|

|

3. GaN LED and AS/P LED Wafer Market Demand (By Region / By Wafer Size)

|

|

4. GaN LED and AS/P LED Wafer Market Demand and Supply Analysis

|

|

LED Player Revenue

and Capacity

|

LED Chip Market Analysis:

|

PDF / Excel

|

2Q (Early Jun.)

4Q (Early Dec.)

|

|

Top 10 LED Chip Manufacturers by Revenue and Wafer Capacity

|

|

LED Package Market Analysis:

|

|

LED Package Manufacturers: Total Revenue, LED Revenue, and Capacity Analysis

|

|

Top 10 LED Package Players by Revenues in Backlight and Flash LED, Lighting, Automotive, Video Wall, UV LED

|

|

LED Industry Price Survey

|

Sapphire / Chip / Package (Backlight, General Lighting, Agricultural Lighting, Automotive, Video Wall, UV LED,

IR LED, VCSEL)

|

Excel

|

1Q (Mid Mar.)

2Q (Early Jun.)

3Q (Early Sep.)

4Q (Early Dec.)

|

|

LED Industry

Quarterly Update

|

Major Players Quarterly Update:

|

PDF

|

1Q (Mid Mar.)

2Q (Early Jun.)

3Q (Early Sep.)

4Q (Early Dec.)

|

|

EU / U.S.- Lumileds, ams OSRAM, Cree LED

(Smart Global Holdings)

|

|

JP- Nichia, Citizen, Stanley, ROHM

|

|

KR- Samsung, Seoul Semiconductor, Seoul Viosys

|

|

ML- Dominant

|

|

TW- Ennostar, Everlight, LITEON, AOT, Harvatek, PlayNitride

|

|

CN- San’an, Changelight, HC SemiTek, Aucksun, Focus Lightings, Nationstar, Hongli, Refond, Jufei, MTC, MLS

|

|

Micro/Mini LED

Exhibit Report

|

CES 2024 / Touch Taiwan 2024

|

PDF

|

Aperiodically;

<20 Pages

|

If you would like to know more details , please contact: