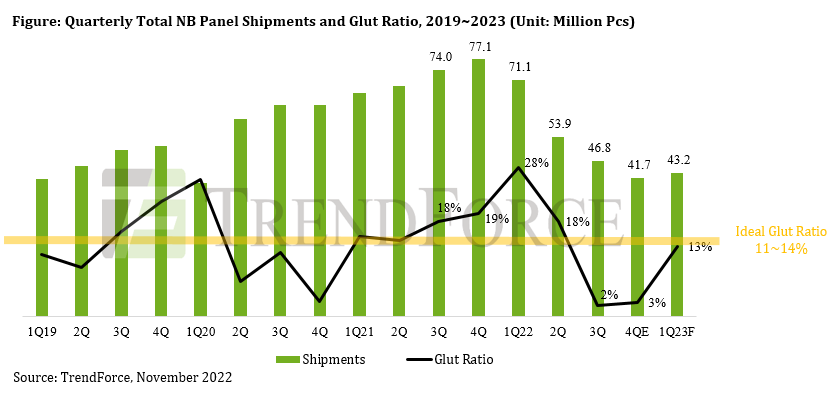

Nov. 28, 2022 ---- TrendForce’s latest research finds that shipments of display panels used in notebook computers (NB panels) came to 13.5 million pieces (pcs) in this October, showing a MoM drop of 16.1% and a YoY drop of 45.0%. Based on TrendForce’s tracking of NB panel shipments, this figure is a 10-year low for the month of October. Moving into 4Q22, TrendForce expects NB panel shipments to remain in a slump because of uncertainties in the global economy and inventory adjustments that are taking place across the entire supply chain. Fourth-quarter shipment figure is now estimated around 41.7 million pcs, reflecting a QoQ drop of 10.8% and a YoY drop of 45.9%.

TrendForce points out that from a historical perspective, this latest decline in NB panel shipments is part of the wider, multi-year cycle for global manufacturing. The cycle first begins with strong demand causing shortages and price hikes. Then, supply outpaces demand, thus leading to falling prices and inventory corrections. Looking back to 2020 when the COVID-19 pandemic was at its height, the surging demand for notebook computers (NBs) caused a panel shortage. Then, even as more panel supply was released, NB brands continued to stock up due to worries about potential shortages of the key components. They allowed their panel inventories to keep climbing. Fast-forward to the recent period, the pandemic has eased, so the supply situation has improved as well. Furthermore, the demand and windfall associated with the effects of the pandemic have also subsided. What follows now is a series of large inventory corrections in the panel market, the kind of which is rarely seen on record in terms of the overall scale.

According to TrendForce’s data, the glut ratio for NB panels reached around 18% in 3Q21. Since the glut ratio for an ideal supply-demand balance should be within 11~14%, the market for NB panels had already shifted to oversupply at that time. This situation was also becoming more severe over the quarters.

Then, moving into 1Q22, the Russia-Ukraine military conflict exacerbated global inflation. Furthermore, China suffered a wave of regional lockdowns as its government enforced a strict zero-COVID policy. These factor together caused a sharp slide in the demand for end products and compelled NB brands to scale back their panel procurements. Consequently, the NB panel market saw falling shipments and glut ratio from 2Q22 onward. Later on, the demand for end products weakened further, and the flow of components and materials was gradually returning normal as the problem of cargo pile-up at the major seaports was easing. Brands thus realized that the massive panel inventory that they had been building up over the preceding quarters had become a serious problem. Now, in the second half of this year, brands have again made considerable cuts to their panel procurement quantities so as to effectively control their inventory levels. The scale of corrections has been reflected by the glut ratio, which has stayed under 5% for two quarters straight (3Q22-4Q22).

In its latest survey of individual brands’ inventory situations for NB panels, TrendForce finds that some US brands began to impose strict inventory control as early as the start of 2Q22. The total NB panel procurement quantity for that quarter saw a QoQ reduction of around 60%. However, the total procurement quantity then rose by around 40% QoQ for 3Q22 as brands’ inventories had fallen back to a relatively healthy level. This dramatic fluctuation between the two quarters indicates that brands will raise demand back up when the inventory situation is again optimal. At the start of 3Q22, brands with a higher inventory level were carrying more than 12 weeks. However, following two quarters of significant adjustments to procurement quantity, more than half of brands are expected to bring their inventories down to the healthy level of 4~8 weeks by the end of this year.

Looking ahead to the first quarter of next year, brands’ procurement quantities will rebound despite the arrival of the low season for end products because their inventory situation is expected to be fairly optimal by then. TrendForce forecasts that NB panel shipments will rise by 3.5% QoQ to 43.2 million pcs for 1Q23. The glut ratio for that quarter will come to around 13%.