According to the latest report of WitsView, a division of TrendForce, global shipments of branded LCD TV sets for 2017 totaled 211 million units, a decrease of 4.1% compared with prior year. This is a new low since 2014, indicating a bottleneck in the development of TV industry. In 2018, TV brands will focus on large-size, high-resolution products, and also develop high-end products like QLED and OLED TVs, hoping to push sales and regain profits by specifications upgrade.

|

|

(Image: LG Display) |

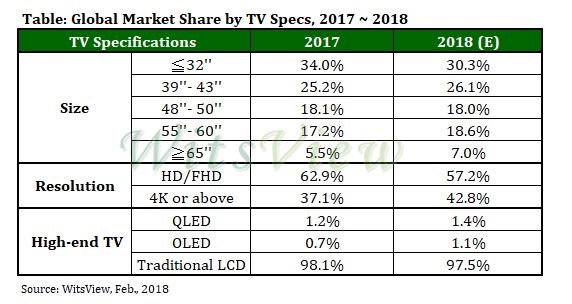

Large-size 4K TV sets have built strong presence in the market, while 8K TVs remain in the early stage of development

In terms of product plans of major TV brands, Samsung, LG and Sony, etc. are now actively developing their product mix of large-size TV sets (65'', 75'' or greater). The proportion of 65'' TVs or greater will increase from 5.5% in 2017 to 7 % this year. BOE Gen 10.5 will offer 65'' and 75'' panels to the market after 1Q18, which may lower TV makers’ costs of purchasing large-size panels.

In terms of resolution upgrade, the market share of high-resolution (4K or higher) products is expected to reach 42.8% this year, up from 37.1% in 2017. In particular, more than 95% of the 55'' or above products use 4K resolution. As the market share of large-size 4K TVs increases, TV vendors have shown a clear ambition to develop 8K resolution. However, as the supply chain for both hardware and software, such as image processing chip, signal interface, 8K signal source and content etc., has not been well developed, WitsView estimates that the penetration rate of 8K products in global TV shipments will be only 0.2-0.3% in 2018. The penetration is expected to increase to 1.5% in 2020 due to the influences of Tokyo Olympics, and to 5% in 2022.

QLED/OLED TVs lead the high-end market, brands are committed to product differentiation

In the high-end market, OLED TVs and QLED TVs remain two competing camps. Led by Samsung Electronics, QLED camp will maintain an overall higher market share than OLED camp. On the other hand, OLED TVs are expected to raise the market share to 1.1% in 2018 since LGD expands its production capacity, gradually narrowing the gap with QLED camp.

As for the future development of high-end TV, QD Pixel, a new technology for QLED camp, is expected to reduce QLED TV's high costs, but its current development remains slow and solutions will be not available until 2019. On the other hand, Gen 10.5 fabs have accelerated the production expansion of large-size LCD panels, lowering the prices as the result. But the costs of OLED panels remain high, and the development of 8K OLED panels remains slow, making OLED TV less competitive in the market. In addition, LGD’s Gen 8.5 OLED fab in Guangzhou will be ready for mass production in 2019, and will face higher depreciation costs.

With the increasingly fierce competition, the TV market is faced with homogeneous products and squeezed profits, so specs upgrade has become the key to driving new purchases and ensuring profitability. Therefore, China's Gen 10.5 or more advanced fabs will play an important role in promoting upgrade of TV size and resolution. In addition, QLED TVs and OLED TVs will also create product differentiation in high-end market, which will bring more highlights to the 2018 TV market.