Near-eye display (NED) devices are primarily developed for two application domains: VR and AR, and OLEDoS technology is advancing its use cases in both.

In the VR market, OLEDoS and LCD can be seen as rivals with comparable performance. LCD technology leverages its relatively mature supply chain and cost structure, currently represented as a cost-effective solution. OLEDoS, on the other hand, offers an advanced and superior technology pathway for VR glasses, featuring high resolution and lightweight design. It is now expected to gain increasing penetration in the VR market.

In the AR market, despite its physical limitations on brightness, OLEDoS has become the mainstream for lightweight immersive-viewing AR glasses due to its high resolution and refresh rate. At early 2026 CES, gaming brand ROG partnered with AR glasses supplier XREAL to launch the ROG XREAL R1 gaming AR glasses with a refresh rate of up to 240 Hz, demonstrating the potential of OLEDoS AR glasses across diverse applications.

Nonetheless, OLEDoS still faces significant challenges in both NED markets. Recently, international brands such as Meta and Apple have reportedly slowed the pace of VR product iterations. Meanwhile, a strategic shift toward AI and AR displays is observed among various brands. Consequently, the opportunities for OLEDoS to gain traction in the VR market has considerably diminished.

The situation is further exacerbated by the fact that even with increased efforts in the AR market, OLEDoS products have not gained growth momentum. For the industry, ideal AR glasses are lightweight eyewear capable of full-day operation and AI integration. Therefore, as the industry holds higher expectations for brightness and transmittance, brand owners are scaling back their investments in viewing products. TrendForce estimates that OLEDoS is likely to experience year-on-year penetration decline in the AR glasses market after 2025.

Although challenged by decreasing market penetration, OLEDoS still exhibits robust momentum in the supply chain. In the Chinese market, capital continues to flow into the OLEDoS industry, with SeeYa, SIDTEK, Metaways, BCDtek, and other Chinese companies ramping up 12-inch production lines. These companies aim to further advance OLEDoS processing technologies and improve yield rates, thereby achieving lower production costs and ultimately leveraging price advantages to enhance OLEDoS’s competitiveness in the NED market.

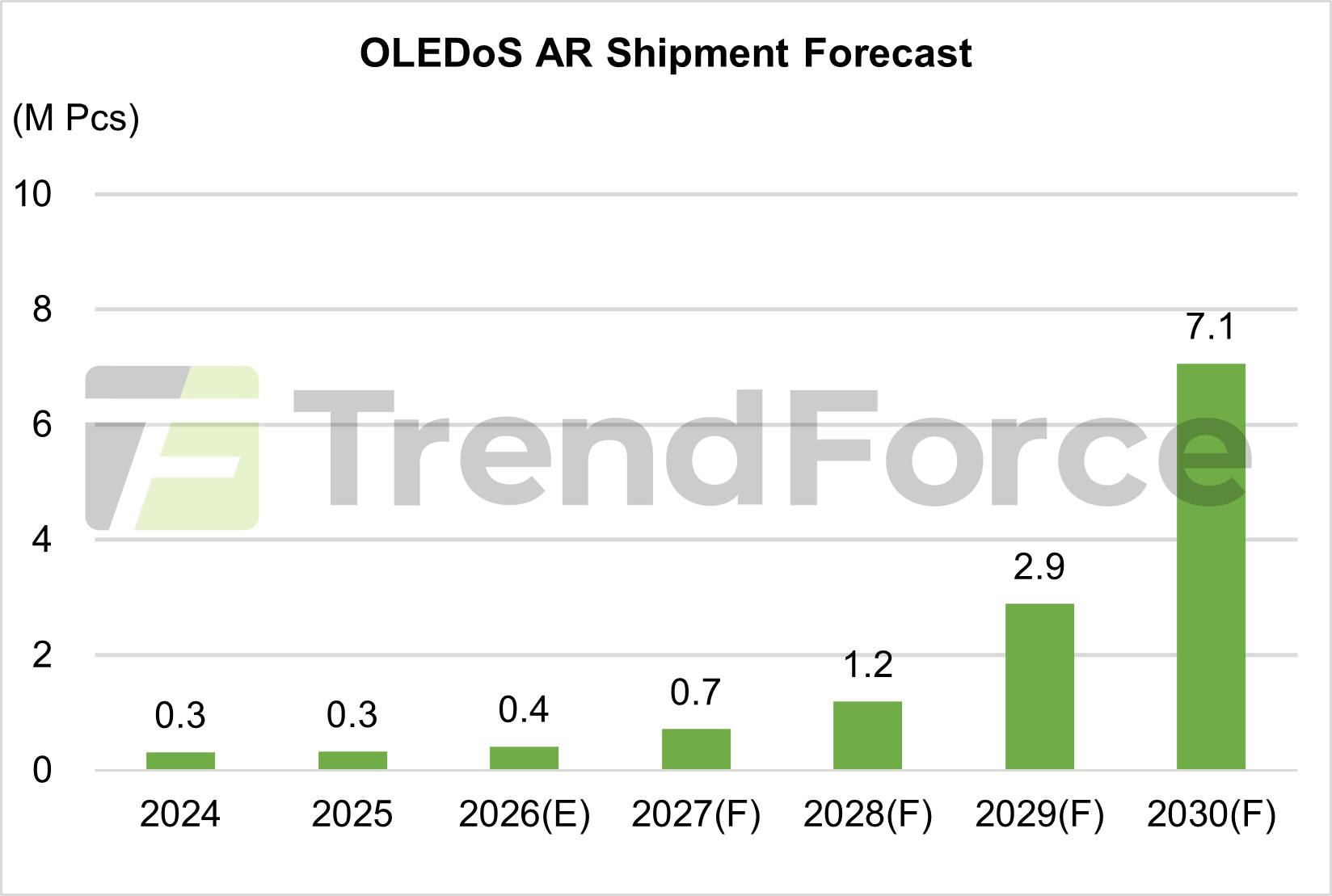

According to TrendForce, OLEDoS is projected to face penetration erosion in the AR domain due to competition from other display technologies such as LEDoS and LCoS. Nonetheless, thanks to the price benefits offered by the aforementioned supply chain developments, more accessible price structures are poised to sustain OLEDoS’s market scale. As the overall AR market volume increases, TrendForce forecasts that shipments of OLEDoS-based AR glasses could hit 7.1 million units by 2030.

Author: Estelle / TrendForce

TrendForce 2025 Near-Eye Display Market Trend and Technology Analysis

Publication Date : 29 August 2025

Language : Traditional Chinese / English

Format : PDF

Page Number: 168

|

If you would like to know more details , please contact:

|